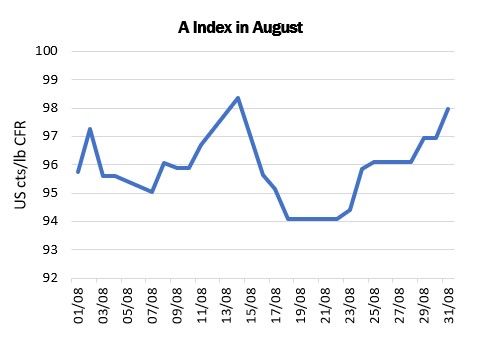

The performance of the Index in August was characterized by two distinct peaks. Led by New York futures, the Index approached the dollar (100 points) but fell both times (a threshold that has not been crossed since early March).

CAUSES:

- Uncertainty about the 23/24 US cotton crop greatly affects market psychology.

- The Ministry of Agriculture has announced a forecast for reduced output. Expected output has fallen from the 16.5 million bales (480 lb) set for July to less than 14 million bales, with drought in West Texas taking a toll on cotton crops (which account for half of the US cotton growing area). ). WASDE’s August report reduced expected US ending stocks from 3.8 to 3.1 million bales.

- Pima fields escaped damage from Tropical Storm Hilary / South Texas was not affected because most of the crop had been harvested -> Crops in the Southeast were less impacted.

- The climate is especially dry in India in August. The impact on cotton production productivity is unclear, but planting is in the final stage -> cotton area will decrease slightly compared to the previous season.

- Pakistan has avoided heavy rains, local forecasts show a strong recovery in output.

- For the African Franc Zone, production forecasts have been revised downward.

CONCLUDE:

A decline (albeit modest) in global raw cotton production is forecast for 2023/24, compared with estimates for 2022/23.

Despite this, the latest estimates suggest that world inventories will increase by more than one million tons by the end of 2023, due to:

- Weakness in world market demand for many months.

- Downstream demand for textiles and garments is weak, yarn sales are stagnant.

- Spinners focus on buying cotton for immediate delivery.

The current cost of replacing raw cotton material is a loss-making proposition if yarn prices do not improve.

CHINA and OTHER MARKETS:

The main import of US and Brazilian cotton is still China, due to:

- Favorable relationship between domestic and international prices.

- U.S. cotton inventories decline ahead of the 2023/24 domestic crop and uncertainty about the size of that crop.

Cotton futures in Zhengzhou continue to show strength, with the spot contract reaching a new high on August 31 (up nearly 4% over the period and more than 24% since the beginning of the year).

A series of auctions by the State Reserve will be launched and import quotas of up to 750,000 tons will be established. Sales from the State Reserve begin on July 31. By the end of August, purchases amounted to more than 250,000 tons, including imported cotton purchased from 2018 to 2022, as well as a small amount of Xinjiang cotton purchased in 2019.

By the end of the month, besides China, Bangladesh showed signs of better raw cotton imports. Ready-made garment export orders and yarn sales volumes and prices obtained have improved. Other markets are also expected to improve.

Cotco (based on Cotlook site)

COTCO stands ready to assist you with any inquiries regarding cotton products. Please don’t hesitate to reach out to us:

☎ +84 (28) 3589 9978 / 3622 2272

📧 trading@cotco-vn.com

#cotton #cotco #cotcocotton #yarn #cotcoyarn #textilemachinery